Free Buyer’s Guide

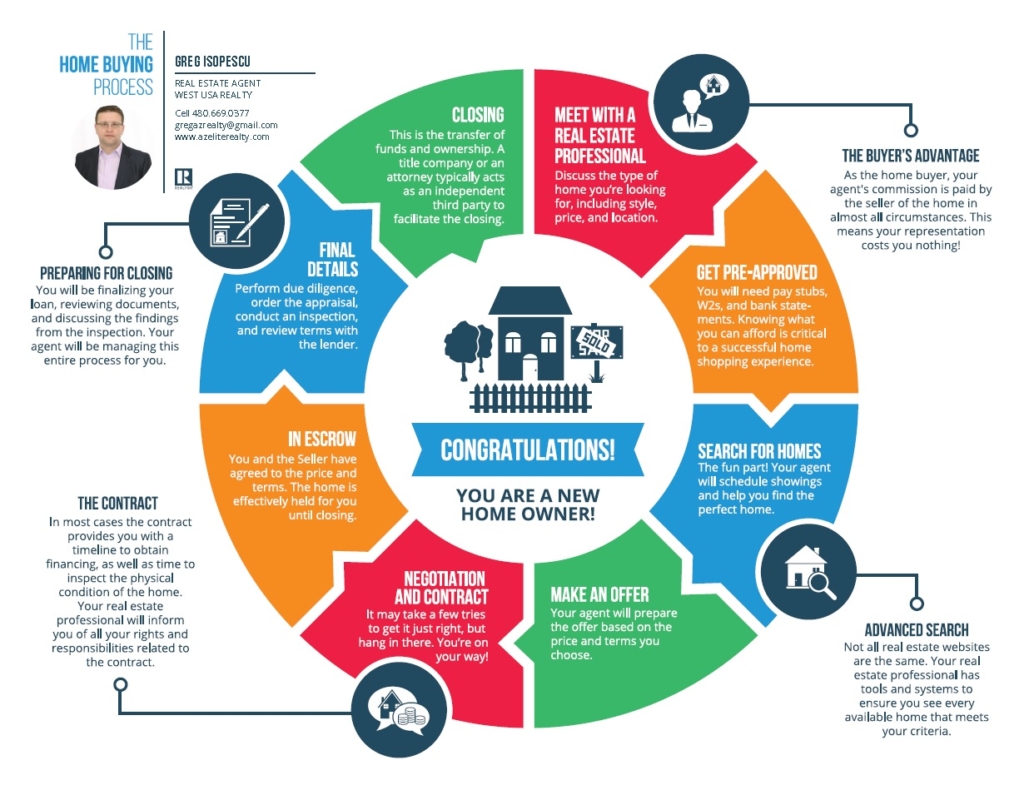

Home Buyer's Roadmap

HOME BUYER 'S ROAD MAP

MODERN BUYER'S PRESENTATION

NEW BUYER QUESTIONNAIRE

REAL ESTATE TERMINOLOGY

HOUSE HUNTING CHECKLIST

Real Estate Terminology

- Adjustable Rate Mortgage (ARM) — The interest rate is tied to a financial index making the monthly mortgage payment go up or down over time.

- Annual Percentage Rate (APR) — The percent of interest the will be charged on a home loan.

- Appraisal — A report highlighting the estimated value of the property completed by a quali- fied 3rd party. This is typically done for the benefit of the buyer to ensure the property is worth what they are paying.

- Association Fee/HOA Fee — In addition to a mortgage, certain housing communities such as townhomes have a monthly fee associated with maintaining the commons areas and ameni- ties.

- Balloon Mortgage — A long-term mortgage loan that starts small but has a large payment due at maturity.

- Closing — This is the final meeting where the buyer and seller signs the necessary paper- work, complete the transaction, and release/take possession of the property. Usually the representing agents and attorneys attend.

- Closing Costs — The buyer and seller have expenses associated with the transaction other than that of the actual cost of the home. For example, the buyer has a variety of fees due for obtaining a new loan and the seller must pay commission to both agents.

- Closing Disclosure — A form that provides the final details about the mortgage loan. It in-cludes loan terms, projected monthly payments, and how much the extra fees will be.

- Collateral — Something of value (in this case your home) that is held to ensure repayment of a mortgage or loan.

- Commission — A percent of the sale price of the home that is paid to agents. The seller pays commission to both the buyer and listing agent.

- Comparables — Homes in the area of interest that have recently sold of which have similar features.

- Contingencies — Conditions which must be met in order to close. Contingencies are typically tied to a date, referred to as a deadline. If the contingency is not satisfied the contract may be canceled.

- Counteroffer — The response from the sellers in regards to an offer.

- Debt to Income Ratio — A lender will look at a borrows debt versus income to determine the amount of loan they are eligible for and if they can repay their debt plus the home loan.

- Down payment — A percent of the cost of the property that is paid up front as a part of the mortgage.

- Earnest Money — The deposit made from the buyer to the seller when submitting an offer. This deposit is typically held in trust by a third party. Upon closing the money will generally be applied to the down payment or closing cost.

- Escrow — This term has multiple meanings; earnest money is typical held by a third party until closing in “escrow”. In can also be referred to as the time period from when the con- tract is written and accepted by the seller to when the home sale actually closes.

- Equity — The difference in the market value of a home versus what is owned on the home.

- FHA — A mortgage that is financed through a private lender and insured by the Federal Housing Administration, often requiring a lower down payment and income to qualify.

- Fixed Rate — The interest rate will remain the same for entire life of the mortgage.

- Home Equity Line of Credit — A loan or line of credit that is determined based on the equity or homes value after subtracting the loans owed.

- Home Inspection — The process in which a professional inspect the seller’s home for issues that are not openly apparent, then creates a report for the buyer to review.

- Home Protection Plan — An annual service that covers the cost of repairs or replacements to items covered in the plan, usually items like stoves, washer/dryers, ect.

- Hybrid — A loan that starts with a fixed rate period, then converts to an adjustable rate.

- Mortgage Insurance — Insurance written in connection with a mortgage loan that protects the lender in the event the borrow cannot repay their loan. This is usually not required if the borrow has 20% or more for the down payment.

- Mortgage Note — A promise to pay a sum of money at a standard interest rate during a specific term and is secured by a mortgage.

- Multiple Listing Service (MLS) — The national list of real estate properties that are available for sale. These are the most reliable sources to receive up-to-date listing information.

- Pre-Approval — The process in which a buyer must provide a mortgage professional the appropriate information on income, debts, and assets that will be used to make the initial credit only loan decision.

- Pre-Qualification — Once approved for a loan, this is the process in which the maximum sale price, loan amount, and month payments are calculated for the borrow. This not a loan approval, however it useful to know prior to searching for a home

- Principal — The underlining amount of the loan which is actually borrowed.

- Property Taxes — These are the taxes that are enforced by the city, town, county, and state government entities. These taxes are included in the total monthly mortgage payments and are held in escrow by the lender.

- REO — Real estate owned properties or foreclosed properties currently owned by a financial institution such as the bank that made the loan to the previous owner

- Reverse Mortgage — This is specifically for seniors and it allows them to convert the equity in their home to cash.

- Short Sale — A situation when the seller’s lender is willing to accept an offer and allows the sale to be completed for an amount less than the mortgage amount owed by the seller.

- Title — A legal document proving current and proper ownership of the property. Also referred to as a Title Deed, this document highlights the history of property ownership and transfers.

- Underwriting — The process in which the potential home buyer is evaluated for their financial ability to obtain and repay a loan, normally consisting of a credit check and appraisal of the property.

- VA Loan — Loans that are given to Americans who have served in the armed forces. They are administered by the Department of Veteran Affairs.